Real Estate Market Update for January 2026: What Buyers and Sellers Need to Know Now

As we close out 2025 and move into 2026, the real estate market is sending a clear message: things are normalizing. That doesn’t mean the market is easy — but it does mean it’s becoming more balanced, more predictable, and more strategic. Both buyers and sellers are navigating a very different lands

Why Waiting for Mortgage Rates to Hit the 5s May Cost You More in Colorado Springs & Monument

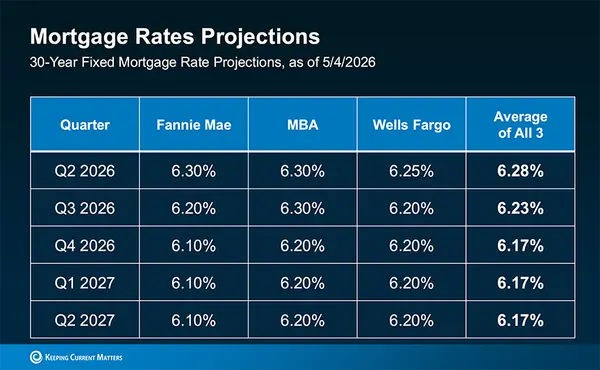

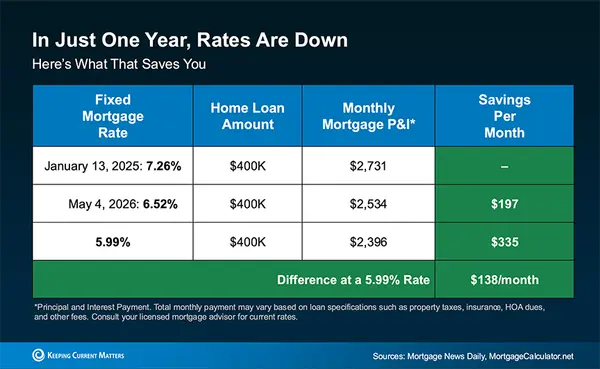

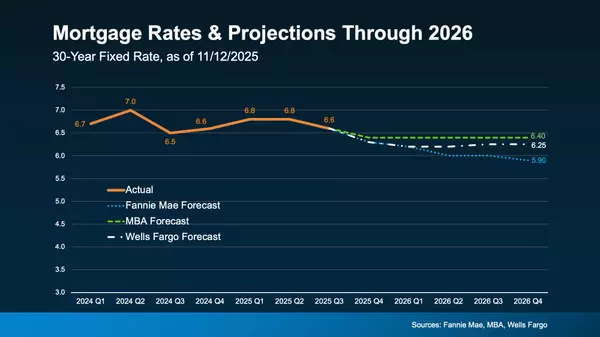

Many home buyers in the Pikes Peak area are actively watching mortgage rates hover just above 6% and thinking, “I’ll buy when rates hit the 5s.” While it seems like a good idea, as who wouldn’t want a lower rate, it actually may not work as you planned.Waiting for 5.99% may not save you as much as y

Prices are Dropping; Why Your Home Equity Still Puts You Way Ahead

If you’ve seen headlines about home prices dropping, it’s easy to wonder what that means for the value of your home too. Here’s what you really need to know. Even with small price declines in the Pikes Peak area, data shows you’re likely still way ahead. With the average appreciation at 5.6% in the

Categories

Recent Posts